My Simple, Stress-Free Plan to Retire Early: Escaping the “Magic Number” Trap #

Meta Description: Stop chasing arbitrary retirement numbers like $2 million. Learn the 5-step stress-free plan to retire early by shifting your focus from net worth to income, mastering the 4% rule, and avoiding common mindset traps.

Introduction: Why You Feel Stuck Despite Saving #

Why do some people with modest savings retire confidently, while others with millions still feel stuck in the corporate grind?

We are often told that retirement requires a staggering, arbitrary amount of money—$1.8 million, $5 million, or even $9 million depending on who you ask. But the reality is that the financial industry thrives on fear, creating an illusion that safety only comes from hitting a massive, often unreachable number.

This guide breaks down the specific mindset traps keeping you employed longer than necessary and provides a concrete, mathematical roadmap to becoming retirement-ready faster than you think.

Part I: The Three Mindset Traps Keeping You From Freedom #

Before we fix the money, we must fix the mindset. If you don’t address these three psychological hurdles, no amount of money will ever feel “safe.”

Trap 1: Safety in Large Numbers (The Moving Goalpost) #

We are terrified of running out of money, so we pick a number that “feels” big and safe rather than calculating what we actually need. The problem is that this number is based on fear, not your actual spending or lifestyle.

- The Result: When you reach your goal (e.g., $1.5 million), fear moves the goalpost to $3 million. You keep working indefinitely because “enough” is always just out of reach.

Trap 2: The “One More Year” Syndrome #

This affects high achievers who are mathematically ready to retire but are paralyzed by anxiety.

-

The Symptoms: You convince yourself you need “just two more bonuses” or “one more year” to be safe.

-

The Reality: This often turns into 5 or 10 years, wasting the healthiest, most energetic years of your early retirement.

-

The Root Cause: It is rarely about money; it is usually fear of losing your identity or not knowing how to fill your day without work structure.

Trap 3: The “False Comparison” Trap #

Many people in their 50s feel “behind” because they compare themselves to internet influencers rather than reality.

-

The Data: The median retirement account for Americans in their 50s is roughly $185,000.

-

The Perspective: If you have $650,000 saved, you have nearly 3.5x the median, yet you may feel impoverished because you are chasing a made-up benchmark.

Part II: The 5-Step Strategy to Retire Early #

The secret to stress-free retirement is shifting your focus from Asset Balance (a static number) to Income Generation (cash flow).

Step 1: Define Your Actual Income Need #

Stop guessing. You must calculate exactly how much income you need to live comfortably.

-

The “Retirement Discount”: Do not assume you need 100% of your current salary. In retirement:

-

You are no longer saving for retirement (that cash flow is freed up).

-

Your taxes should be dramatically lower.

-

Your mortgage and other debts may be paid off.

-

-

Action: Audit your bank statements for the last 3–6 months to find your true “freedom number.”

Step 2: Calculate Your Guaranteed Income #

Identify income sources that do not rely on the stock market.

-

Social Security: Check the SSA website for your estimated benefit.

-

Pensions: Confirm the exact annual payout with your provider.

Step 3: Do the “Gap Math” (The 4% Rule) #

Once you know your total need and your guaranteed income, your portfolio only needs to cover the difference. We use the 4% Rule to determine the portfolio size required to generate that income safely.

The Formula:

$$\text{Portfolio Needed} = \frac{\text{Annual Income Gap}}{0.04}$$The Example:

-

Comfortable Living Cost: $60,000 / year.

-

Guaranteed Income (SS + Pension): $30,000 / year.

-

Income Gap (Portfolio Withdrawal): $30,000 / year.

- The Insight: You do not need $2 million. You need $750,000. If you have a larger pension, you might only need $375,000. When you do the math, the mountain becomes climbable.

Step 4: Protect Against the “Danger Zone” #

The most critical period is the Retirement Danger Zone: the decade leading up to retirement and the decade following it.

-

The Risk: If a market crash happens immediately after you retire (Sequence of Returns Risk), withdrawing money from a declining portfolio can destroy your long-term wealth.

-

The Solution: Build a “Safe Bucket.” In your final working years, shift a portion of your portfolio into defensive assets like bonds or fixed income.

-

How it Works: If the market crashes, you spend your “bond money,” leaving your stocks untouched to recover.

Step 5: The “Secret Hack” – Partial Retirement #

If the math is tight or you are scared of boredom, consider transitioning from full-time to part-time, consulting, or freelance work.

-

Benefits:

-

It reduces the withdrawal pressure on your portfolio.

-

It solves the identity crisis by keeping you engaged.

-

It serves as a “stress test” for your retirement lifestyle.

-

Part III: Answering the “What Ifs” #

“What if I live to 100?” #

Many fear living too long will drain their funds. However, if your portfolio is invested properly, longevity is actually an advantage.

-

Compounding: Because the market (historically growing at ~10%) generally outpaces a 4% withdrawal rate, your portfolio should theoretically continue to grow.

-

Outcome: You will likely be richer at 90 than you were at 60.

“What about unexpected expenses?” #

Do not let “what ifs” paralyze you.

- Budget for Stress: Instead of staying in a job you hate just in case, build a buffer into your financial plan or use planning software to “stress test” different market scenarios.

Conclusion: It’s Not Luck, It’s a Plan #

People who retire early and confidently are not “lucky” and they are not taking crazy risks. They simply stopped obsessing over a random net worth number and started planning for income.

Your Next Step: Sit down this week and perform the “Income Audit.” Calculate your actual spending needs versus your guaranteed income. The gap might be much smaller than you think—and your freedom might be much closer than you realize.

Action Plan Checklist #

-

Review 6 months of expenses to determine your true annual cost of living.

-

Log in to the Social Security website to confirm your future benefits.

-

Apply the 4% Rule: Divide your annual income gap by 0.04.

-

Assess your Asset Allocation: If you are within 10 years of retiring, ensure you have a “safe bucket” (bonds/cash).

-

Define your “New Identity”: List 3 things you will do in retirement to replace the structure of work.

New : #

Are you exhausted from the relentless 9-to-5 routine and yearning for a life where financial worries don’t dictate your days? Early retirement through the FIRE (Financial Independence, Retire Early) movement isn’t reserved for millionaires—it’s within reach for anyone willing to adopt a straightforward, low-stress approach. As a seasoned personal finance expert, I’ve helped countless individuals craft plans that prioritize simplicity, smart habits, and long-term peace of mind. In this guide, I’ll outline my proven, stress-free strategy to retire early, drawing on principles like disciplined saving, wise investing, and balanced living. No matter if you’re starting in your 20s or catching up in your 40s, this plan empowers you to build wealth steadily and reclaim your time.

We’ll cover assessing your finances, setting realistic goals, optimizing your budget, investing effectively, creating passive income, and addressing common challenges—including often-overlooked aspects like healthcare, taxes, and market risks. Packed with actionable steps, real examples, and expert insights, this post is your roadmap if you’re googling “how to retire early on a budget,” “FIRE strategies for beginners,” or “stress-free early retirement plan.” Let’s make financial independence feel achievable and exciting.

Why Pursue Early Retirement? Unlocking the True Rewards of FIRE #

Early retirement is more than escaping work—it’s about designing a life of purpose, health, and joy without financial chains. FIRE enthusiasts frequently highlight how ditching the grind leads to profound well-being improvements, from stronger relationships to personal growth.

Here are the standout benefits:

- Ultimate Freedom: Imagine traveling spontaneously, volunteering for causes you love, or diving into hobbies like painting or hiking—free from office demands.

- Health Boost: Chronic job stress ages us prematurely, per research in the Journal of Occupational Health Psychology. Early retirees often enjoy better mental and physical health with time for exercise and relaxation.

- Bulletproof Security: Passive income streams act as a buffer against recessions, inflation, or unexpected costs, ensuring stability.

- The Power of Compounding: Time is your ally; modest early savings can snowball into millions thanks to investment growth.

Wondering if early retirement works on an average salary? Absolutely—many achieve it earning $50,000–$80,000 annually through consistent, low-effort habits. The key? Starting now with a plan that feels manageable, not overwhelming.

Action Checklist for Motivation #

- Reflect on your “why”: Journal three non-work activities you’d pursue in retirement.

- Join a FIRE community like Reddit’s r/financialindependence for inspiration.

- Calculate a quick win: Use an online compound interest calculator to see how $200/month grows over 20 years at 7% returns.

Step 1: Take Stock of Your Finances—Your Stress-Free Starting Point #

Every solid plan begins with clarity. Assessing your current situation removes the anxiety of unknowns and sets a factual foundation. Think of this as a gentle financial check-up, not an audit.

Key Elements to Evaluate #

- Net Worth Snapshot: Assets (cash, stocks, property) minus debts (loans, credit cards). Tools like Mint or Personal Capital make this effortless.

- Expense Tracking: Monitor spending for 1–3 months via apps like YNAB. Categorize into essentials (50%), discretionary (30%), and savings (20%).

- Savings Rate Calculation: Savings divided by after-tax income. Target 50%+ for accelerated FIRE—achievable by trimming luxuries like subscriptions.

- Debt Review: Tackle high-interest debts first (e.g., credit cards at 15%+ APR) using the avalanche method for quickest payoff.

Expert Insight #

As Ramit Sethi advises, treat your finances like a business CEO would—data-driven and proactive. This step ensures your plan aligns with reality, reducing future surprises.

Action Plan #

- Download a tracking app and log expenses today.

- Compute your net worth in under 30 minutes.

- Identify one high-interest debt to prioritize.

- Celebrate small insights to keep momentum positive.

Step 2: Craft Your Personalized FIRE Goal—The “Number” That Sets You Free #

Define success early to stay motivated. Your “FI number” is the nest egg needed for sustainable withdrawals, typically using the 4% rule (annual expenses x 25). For $40,000 yearly spending, aim for $1 million—but adjust for your lifestyle.

Calculating Your FI Number #

- Project retirement expenses: Include inflation (assume 3% yearly) and shifts like reduced work costs or increased travel.

- Leverage tools: Vanguard’s Retirement Calculator or FIRECalc for simulations incorporating market variability.

Timeline Strategies #

- Aggressive Path (10–15 Years): Save 50–70% of income for rapid progress.

- Balanced Path (15–25 Years): 30–50% savings for a gentler pace.

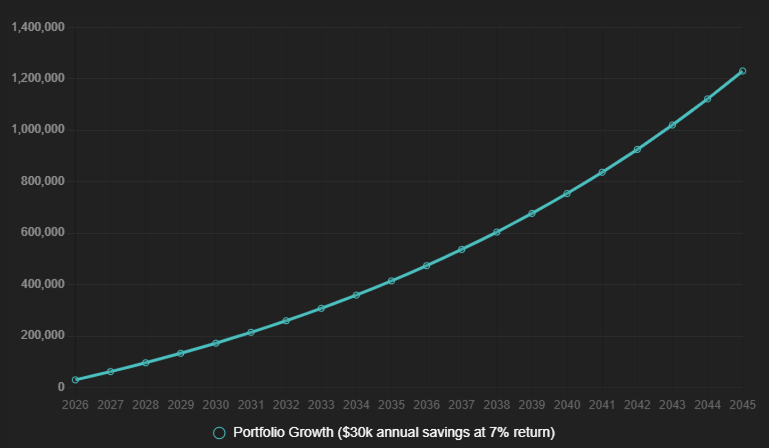

- Real Example: A 30-year-old earning $60,000 saving 50% ($30,000/year) could hit $1 million by 45 at 7% average returns (inflation-adjusted).

To visualize, here’s a sample growth trajectory for that scenario:

Buffers for Peace of Mind #

- Inflation and Healthcare: Budget $500–$1,000/month for pre-Medicare insurance.

- Safety Margins: Add 20–30% extra to your FI number for downturns or longevity.

This goal-setting keeps things stress-free by breaking the journey into milestones, like hitting 25% of your number first.

Action Plan #

- Use a calculator to estimate your FI number.

- Set 1-, 5-, and 10-year targets.

- Review annually, adjusting for life changes.

Step 3: Widen Your Wealth Gap—Boost Income, Trim Expenses Effortlessly #

The FIRE engine? Maximizing the difference between what you earn and spend. Focus on joyful optimizations, not deprivation.

Income Acceleration Tips #

- Side Gigs: Freelance via Upwork or blog for $500–$2,000/month extra.

- Career Moves: Negotiate 5–10% raises or job-hop for 15–20% boosts.

- Passive Builders: Start with dividend investments or peer-to-peer lending.

Expense Optimization Without Pain #

- Housing Hacks: House-hack by renting rooms to cap at 25–30% of income.

- Daily Wins: Meal prep to save $200/month; cycle or use transit over cars.

- Minimalist Mindset: Embrace Marie Kondo—keep only what sparks joy to curb shopping.

Mr. Money Mustache calls frugality “luxury on the cheap,” turning savings into fun challenges.

| Savings Rate | Years to FI (Assuming 7% Returns) |

|---|---|

| 20% | 37 years |

| 30% | 28 years |

| 50% | 17 years |

| 70% | 9 years |

Action Plan #

- Audit expenses and cut one category by 10%.

- Automate transfers to high-yield savings (e.g., Ally at 3.30% APY).

- Launch a low-effort side hustle this month.

Step 4: Invest Smartly—Let Your Money Work for You #

Investing fuels growth, but keep it simple to avoid stress. Prioritize low-fee, diversified options.

Core Strategies #

- Funds for Beginners: Vanguard VTSAX (0.04% fees) for market-wide exposure.

- Allocation Basics: 80/20 stocks/bonds, shifting conservatively with age (e.g., 110 – your age in stocks).

- Tax-Smart Accounts: Max 401(k)s ($23,500 limit in 2025), IRAs ($7,000 under 50), and HSAs.fidelity.comfidelity.com

Navigating Ups and Downs #

- Dollar-cost average to buy steadily.

- Rebalance yearly; ignore daily noise.

- Historical S&P 500 real returns: ~7% annually.tradethatswing.com

Read JL Collins’ “The Simple Path to Wealth” for timeless principles.

Action Plan #

- Open a brokerage account if needed.

- Set up automatic investments.

- Educate via one book or podcast episode.

Step 5: Secure Passive Income and Safety Nets #

Sustain retirement without eroding capital through diversified streams.

Income Ideas #

- REITs: VNQ for real estate without management.

- Dividends: Reliable picks like Johnson & Johnson (2.5% yield).stockanalysis.com

- Digital Assets: Sell e-books or courses on Etsy.

Essential Safeguards #

- Emergency Fund: 6–12 months in liquid accounts.

- Insurance: Comprehensive coverage for life and disability.

- Test Run: Live on your projected budget for a month.

Action Plan #

- Build toward 3–5 streams.

- Consult a lawyer for asset protection (e.g., LLCs).

- Simulate retirement quarterly.

Step 6: Plan for Healthcare, Taxes, and Risks—The Overlooked Essentials #

To keep it truly stress-free, address these gaps head-on.

- Healthcare Strategies: Pre-65? Use ACA subsidies or HSAs (tax-free for medical). Post-65: Medicare supplements.

- Tax Optimization: Favor Roth accounts for tax-free growth; consider conversions to minimize future burdens.

- Risk Management: Guard against sequence of returns risk by holding 2–3 years’ expenses in cash/bonds during early retirement.

These additions ensure longevity, per experts like Vicki Robin.

Action Plan #

- Research ACA options in your state.

- Meet with a tax advisor.

- Build a cash buffer.

Overcoming Common Hurdles: Stay on Track Without Stress #

Challenges arise, but preparation turns them into minor bumps.

- Inflation: Invest in TIPS or stocks for growth.

- Market Dips: Stick to your plan; history shows recoveries.

- Lifestyle Creep or Boredom: Set spending guardrails and plan fulfilling activities.

Final Thoughts: Embark on Your Stress-Free FIRE Journey #

This simple plan—assess, goal-set, optimize, invest, secure passives, and plan holistically—leads to early retirement without overwhelm. Consistency beats intensity; start with one step today, like automating $100 in savings, and let compounding do the rest. You’re capable of this freedom—embrace it.

Share your first action in the comments, and subscribe for more FIRE wisdom. For tailored guidance, consult a financial planner.

SEO Keywords: early retirement plan, how to retire early, FIRE strategies, stress-free financial independence, retire early on average salary