Before We Begin: Capital Requirements #

Capital Reality Check

One major advantage of SPY over SPX: you need far less capital to trade effectively.

| Capital Level | What’s Possible with SPY Iron Condors |

|---|---|

| $10,000 - $25,000 | Can trade 1-3 contracts. Good for learning, but one loss stings. |

| $25,000 - $50,000 | Workable. Run 3-6 positions monthly with proper risk management. |

| $50,000 - $100,000 | Optimal for SPY. Full diversification, 5-10 positions, 25% cash buffer. |

| $100,000+ | Consider graduating to SPX for tax advantages and lower relative commissions. |

Why SPY specifically? The most liquid security on the planet. Tightest bid-ask spreads you’ll find ($0.01-$0.05). Position sizes 1/10 of SPX, giving you precise control over risk.

Why I Chose SPY Over SPX for Iron Condors #

I spent months analyzing both. Here’s why I landed on SPY:

Why SPY Wins for Most Traders #

| Factor | SPY Reality |

|---|---|

| <span | |

| class=“rounded-md border border-primary-400 px-1 py-[1px] text-xs font-normal text-primary-700 dark:border-primary-600 dark:text-primary-400”> | |

| Unmatched Liquidity | |

| Millions of contracts daily. Spreads of $0.01-$0.05. You always get filled. | | Flexible Sizing

| 1 contract = ~$590 collateral. Scale precisely with your account. | | Easier Adjustments

| Rolling one contract at a time is simple. SPX forces chunky moves. | | Lower Capital Barrier

| Start with $25k. SPX realistically needs $100k+. | | Weekly Options

| M/W/F expirations give flexibility. Daily on SPX feels like gambling. |

What I Give Up by Using SPY #

| Factor | SPX Advantage | My Response |

|---|---|---|

| Cash Settlement | No assignment risk | I manage around this—rarely an issue |

| 60/40 Tax Treatment | Better for high earners | My IRA doesn’t care about taxes |

| Commission Efficiency | Lower per-notional on large accounts | SPY commissions are still tiny |

When to consider SPX: Taxable account with $200k+, where 60/40 treatment saves meaningful money.

What Research Shows #

From projectfinance analysis of 71,417 iron condor trades:

| Metric | SPY Results |

|---|---|

| Win Rate (16-delta, 45 DTE) | 77.6% |

| Avg P/L per Contract | $35.39 when held to expiration |

| Best Management | Close at 50% profit: 89% win rate |

Critical finding: Spintwig research shows the call side of index iron condors has historically been unprofitable. The edge is primarily on the put side. This applies to both SPY and SPX.

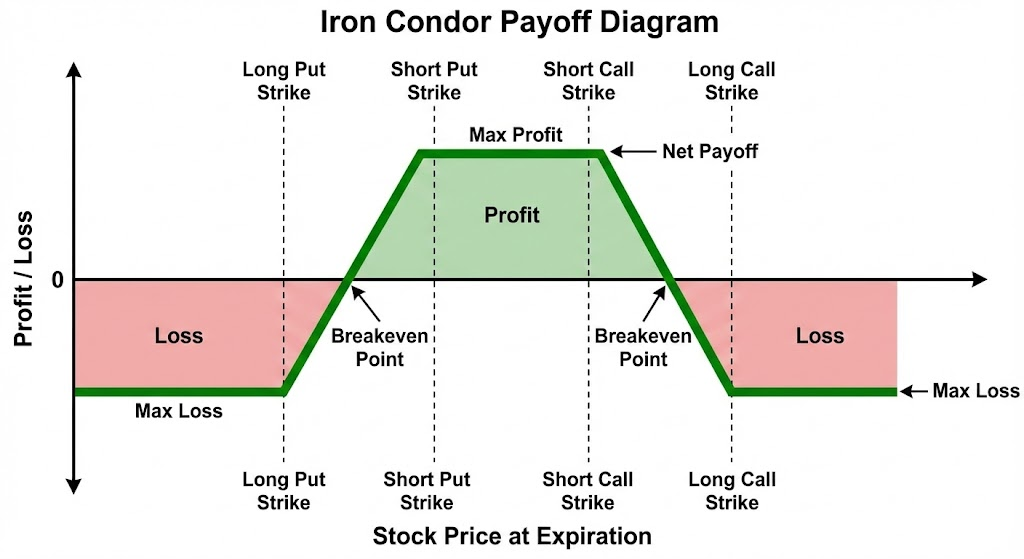

Understanding Iron Condors: The Mechanics #

An Iron Condor combines two credit spreads—one above the current price, one below—creating a “profitable zone” where I keep my premium.

The Structure #

graph TD

subgraph "BEAR CALL SPREAD (Above Market)"

A[Buy Call @ 620

Long Protection] --> B[Sell Call @ 615

Short Strike]

end

subgraph "CURRENT MARKET"

C[SPY @ 594

Current Price]

end

subgraph "BULL PUT SPREAD (Below Market)"

D[Sell Put @ 570

Short Strike] --> E[Buy Put @ 565

Long Protection]

end

B -->|Premium Collected| F[Total Credit

= Max Profit]

D -->|Premium Collected| F

style C fill:#1e3a5f,stroke:#60a5fa,color:#e2e8f0

style F fill:#0f5132,stroke:#75b798,color:#d1e7dd

The Four Legs Explained #

| Leg | Action | Example Strike | Purpose |

|---|---|---|---|

| 1. Long Put | Buy | $565 | Defines max loss on downside (protection) |

| 2. Short Put | Sell | $570 | Collects premium below market |

| 3. Short Call | Sell | $615 | Collects premium above market |

| 4. Long Call | Buy | $620 | Defines max loss on upside (protection) |

Wing Width: In this example, both spreads are $5 wide. Wider wings = more premium but more max loss.

My Real Trade Example: January 2026 #

Here’s an actual Iron Condor setup based on current market conditions (SPY ~$594, VIX ~15.5):

Live Example: 45-DTE Iron Condor (March 7, 2026 Expiration)

| Component | Details |

|---|---|

| Underlying | SPY @ $594 |

| VIX Level | 15.5 |

| Expiration | 45 DTE (March 7, 2026) |

Bull Put Spread (Below Market):

- Sell $570 Put @ $1.45 credit

- Buy $565 Put @ $1.10 debit

- Net Credit: $0.35 ($35/contract)

Bear Call Spread (Above Market):

- Sell $615 Call @ $1.20 credit

- Buy $620 Call @ $0.85 debit

- Net Credit: $0.35 ($35/contract)

Combined Position:

| Metric | Value |

|---|---|

| Total Net Credit | $0.70 ($70/contract) |

| Max Profit | $70 (if SPY between $570-$615 at expiration) |

| Max Loss | $5 width - $0.70 credit = $4.30 ($430/contract) |

| Lower Breakeven | $570 - $0.70 = $569.30 |

| Upper Breakeven | $615 + $0.70 = $615.70 |

| Profitable Range | 4.2% below to 3.7% above current price |

| Probability of Profit | ~72% (both short strikes ~0.16 delta) |

| Risk/Reward Ratio | 6.1:1 (risk $430 to make $70) |

Understanding the Risk/Reward #

Yes, you read that right—I risk $430 to make $70. That’s a 6:1 ratio against me. Here’s why it still works:

The Math That Makes It Work

| Metric | Value | Explanation |

|---|---|---|

| Win Rate | ~72% | Out of 100 trades, I win ~72 |

| Expected Win | 72 × $70 = $5,040 | Total from winners |

| Expected Loss | 28 × $430 = $12,040 | Total from losers |

| Gross Expectancy | -$7,000??? | Wait, that’s negative! |

But here’s the key: I don’t hold to expiration or max loss. With active management:

- Close winners at 50% profit ($35) → 89% win rate

- Close losers at 2x credit ($140 loss) → Limited damage

Managed Expectancy:

- 89 wins × $35 = $3,115

- 11 losses × $140 = $1,540

- Net Expected: +$1,575 per 100 trades = +$15.75/trade

Payoff Diagram #

Backtested Performance: What the Data Shows #

I’ve studied the historical performance of SPY Iron Condors extensively. Here’s what decades of data reveal:

Historical Backtest Results #

SPY Iron Condor Performance (Research Compilation)

| Strategy Variation | Win Rate | Avg Return/Trade | Annual Return | Max Drawdown |

|---|---|---|---|---|

| Hold to Expiration | 77.6% | $35.39 | 12-15% | -25 to -35% |

| Close at 50% Profit | 89% | ~$25-30 | 15-20% | -15 to -20% |

| Close at 50% OR 21 DTE | 85% | ~$20-25 | 14-18% | -12 to -18% |

Sources: projectfinance, Spintwig, Market Chameleon

The Volatility Risk Premium Edge #

The fundamental edge: Implied Volatility consistently exceeds Realized Volatility on average.

graph LR

A[VIX = 15.5

What Options Price In] -->|"Fear Premium"| B[Edge for Sellers]

C[Realized Vol = 10-12%

What Actually Happens] -->|"Reality"| B

B --> D[~4-6% VRP

My Edge]

style D fill:#0f5132,stroke:#75b798,color:#d1e7dd

When I sell an Iron Condor, I’m selling insurance at inflated prices. Over time, the market doesn’t move as much as options prices imply—that’s my edge.

Critical Research Warning #

The Call Side Problem

From Spintwig backtests:

“Research suggests that 45-DTE short SPX calls have generally experienced a negative expected value. Since the call side of a short iron condor is systematically unprofitable, it would make sense to simply sell the put only.”

What this means: The iron condor’s edge comes almost entirely from the put spread. The call spread is more of a “hedge” against upside moves than a profit center.

My approach: I still trade full iron condors because:

- The call credit offsets some put-side losses

- It reduces my directional exposure

- In certain volatility regimes, calls outperform

But I’m aware the put side does the heavy lifting.

My Optimal Setup Parameters #

After studying the research and trading live, here are my preferred parameters:

The Sweet Spot Configuration #

| Parameter | My Setting | Why |

|---|---|---|

| DTE (Days to Expiration) | 30-45 days | Optimal theta decay, manageable gamma |

| Short Strike Delta | 0.14-0.18 | ~82-86% probability OTM each side |

| Wing Width | $5 on SPY | Defines max loss, balances premium vs risk |

| Premium Target | ≥ 12% of wing width | $5 wings → minimum $0.60 credit |

| VIX Range | 14-25 | Premium attractive but not signaling crisis |

| Max Position Size | 3-5% of portfolio | One position won’t ruin me |

| Max Concurrent Positions | 4-6 | Spread across expirations |

Delta Selection Guide #

graph LR

A[0.08 Delta

92% Win Rate] --> B[Premium: ~$0.40

Too Thin]

C[0.12 Delta

88% Win Rate] --> D[Premium: ~$0.55

Acceptable]

E[0.16 Delta

84% Win Rate] --> F[Premium: ~$0.70

MY SWEET SPOT]

G[0.20 Delta

80% Win Rate] --> H[Premium: ~$0.90

Tastytrade Standard]

I[0.30+ Delta

70% Win Rate] --> J[Premium: ~$1.40

TOO AGGRESSIVE]

style E fill:#0f5132,stroke:#75b798,color:#d1e7dd

style G fill:#664d03,stroke:#ffc107,color:#fff3cd

style I fill:#842029,stroke:#ea868f,color:#f8d7da

Width Selection Trade-offs #

| Wing Width | Max Loss/Contract | Typical Premium | Premium % | My Take |

|---|---|---|---|---|

| $2 | $200 | $0.25-0.35 | 12-17% | Too small, poor risk/reward |

| $5 | $500 | $0.60-0.80 | 12-16% | My standard |

| $10 | $1,000 | $1.20-1.60 | 12-16% | Good for larger accounts |

| $20 | $2,000 | $2.40-3.20 | 12-16% | Capital intensive |

Position Management: My Rules #

Take Profit Rules #

When to Close for Profit:

| Trigger | Action | Why |

|---|---|---|

| 50% of max profit reached | Close entire position | Lock in gains, free up capital |

| 21 DTE remaining | Close if profitable | Gamma risk accelerates |

| 70% profit + <14 DTE | Close immediately | Diminishing risk/reward |

Example: Received $0.70 credit. When I can buy it back for $0.35 or less, I close and redeploy capital to next month’s condor.

Research backing: Projectfinance found that closing at 50% profit increased win rate from 77.6% to 89%.

Adjustment Rules: When Things Go Wrong #

Rolling the Untested Side

When SPY moves toward one short strike, I “roll” the opposite (untested) side closer to collect additional credit:

Scenario: SPY drops from $594 toward $575 (approaching my $570 put strike).

- My $615 call spread is safe (untested, worth nearly $0)

- Action: Buy back the $615/$620 call spread for ~$0.05, sell a new $595/$600 call spread for ~$0.25

- Result: Extra $0.20 credit, lower upper breakeven, wider put-side cushion

Rules for Rolling:

- Only roll for a NET CREDIT (never pay to adjust)

- Don’t extend beyond 60 DTE total duration

- Maximum 2 adjustments per trade

- If short strike is breached, consider closing at defined loss

Reference: Tastytrade rolling guide

Stop Loss Rules #

When to Take a Loss:

| Condition | Action | Rationale |

|---|---|---|

| Loss = 2x credit received | Close immediately | Defined loss point |

| Short strike breached | Evaluate closing | Probability shifts against you |

| VIX spikes >25 intraday | Tighten stops | Vol expansion hurts |

| <7 DTE and tested | Close regardless | Gamma will accelerate losses |

My Hard Rule: Never let a single Iron Condor lose more than 2% of my total portfolio. On $50k, that’s $1,000 max loss per position.

Position sizing math: With $5 wings ($500 max loss per contract), I trade 2 contracts max to stay within my 2% rule.

The Greeks: What I Monitor #

Critical Greeks Exposure #

| Greek | Iron Condor Exposure | Practical Meaning |

|---|---|---|

| Delta | Near zero (neutral) | I’m not betting on direction |

| Theta | Positive (+) | Time decay earns me $5-15/day per position |

| Vega | Negative (-) | If VIX rises, my position loses value |

| Gamma | Negative (-) | Large moves hurt; accelerates near expiration |

My Daily Check (Under 5 Minutes) #

graph TD

A[Daily Check] --> B{Position Delta > ±0.15?}

B -->|No| C[No Action Needed]

B -->|Yes| D[Consider Rolling Untested Side]

A --> E{DTE Remaining?}

E -->|> 21 DTE| F[Weekly Check OK]

E -->|≤ 21 DTE| G[Daily Monitoring Required]

A --> H{Current P/L?}

H -->|≥ 50% Profit| I[CLOSE POSITION]

H -->|Loss ≥ 2x Credit| J[CLOSE POSITION]

H -->|Between| K[Hold and Monitor]

style I fill:#0f5132,stroke:#75b798,color:#d1e7dd

style J fill:#842029,stroke:#ea868f,color:#f8d7da

Realistic Return Expectations #

Let me be completely honest about what’s achievable:

My Monthly Target Model ($50k Account) #

Conservative SPY Iron Condor Model

Per Trade Setup:

- Capital allocated: $1,000-1,500 (2-3 contracts × $500 max loss)

- Credit received: $140-210 ($70/contract × 2-3)

- Target profit (50%): $70-105

Monthly Activity:

| Month Type | Trades | Wins | Losses | Net Result |

|---|---|---|---|---|

| Good Month | 3 | 3 | 0 | +$210-315 |

| Average Month | 3 | 2 | 1 | +$0 to +$70 |

| Bad Month | 3 | 1 | 2 | -$140 to -$280 |

Annual Projection (Conservative):

- Good months: 5 × $250 = $1,250

- Average months: 5 × $35 = $175

- Bad months: 2 × -$200 = -$400

- Net Annual: ~$1,025 = ~2% on $50k

Wait, only 2%? That’s the conservative, fully-managed approach. Scale up position sizes (within risk rules) and you can reach 8-15% annually. But I’d rather underpromise and overdeliver.

Scaling the Strategy #

| Account Size | Contracts/Trade | Monthly Trades | Annual Target |

|---|---|---|---|

| $25,000 | 1-2 | 2-3 | $500-1,500 (2-6%) |

| $50,000 | 2-4 | 3-4 | $1,500-4,000 (3-8%) |

| $100,000 | 4-8 | 4-5 | $4,000-10,000 (4-10%) |

| $200,000+ | Consider SPX | 4-6 | $10,000-25,000 (5-12%) |

Visual: Compound Growth Scenarios #

Iron Condors vs. My CSP Strategy #

How do Iron Condors fit into my overall options portfolio?

| Factor | Iron Condors (SPY) | Cash Secured Puts | Winner For… |

|---|---|---|---|

| Market Bias | Neutral | Bullish/Neutral | CSPs in uptrends |

| Max Loss | CAPPED ($430/contract) | Strike × 100 (large) | Iron Condors |

| Best Environment | Low vol, range-bound | Dips, high IV | Depends on market |

| Win Rate | 70-85% | 80-85% | Similar |

| Capital Efficiency | Good ($500/contract) | Lower ($5,000+/contract) | Iron Condors |

| Stress Level | Medium (4 legs to watch) | Low (2 legs) | CSPs |

| Adjustment Complexity | Higher | Lower | CSPs |

My Current Allocation:

- 60% Cash Secured Puts on quality stocks (bullish conviction)

- 30% Iron Condors on SPY (neutral income)

- 10% Cash buffer for opportunities

Common Mistakes I’ve Made (Learn From Them) #

My Expensive Lessons:

| Mistake | What Happened | How I Fixed It |

|---|---|---|

| Holding to expiration | Watched 80% profit turn into loss | Now close at 50% profit religiously |

| Too tight strikes | High premium but constant breaches | Moved to 0.14-0.18 delta |

| No adjustment plan | Panic closed at worst times | Pre-defined rolling rules |

| Trading in high VIX | Thought “more premium = better” | Now avoid VIX > 25 entries |

| Too many positions | Couldn’t manage them all | Max 4-6 concurrent |

| Ignoring the call side research | Expected both sides to contribute | Accept puts carry the edge |

When NOT to Trade Iron Condors #

I Skip Iron Condors When:

| Condition | Why I Avoid |

|---|---|

| VIX > 28 | Vol spikes mean trending moves, not ranges |

| VIX < 12 | Premiums too thin to justify the risk |

| SPY below 200-day MA | Bear market = trending, not ranging |

| Major event in 48h | FOMC, CPI, jobs report = unpredictable gaps |

| Earnings season peak | Sector rotations cause correlation breakdowns |

| Already have 6+ positions | Can’t manage more effectively |

Related Resources #

I’ve created detailed execution guides for this strategy:

Essential Iron Condor Resources

📋 Iron Condor Entry Checklist - Every criterion must pass before trading. Print this.

📊 Iron Condor Workflow Guide - Daily/weekly routine, adjustment mechanics, position tracking.

📄 Iron Condor 1-Page SOP - The entire system on one printable page.

The Bottom Line #

My Fundamental Philosophy

I’m not predicting where SPY will go. I’m betting it won’t go as far as the options market thinks it will.

That’s the volatility risk premium in action. Most months, I’m right. Some months, I’m wrong. But over time, the math works.

What Iron Condors on SPY give me:

- Defined risk (I know my max loss before entering)

- Neutral stance (I don’t need to be right about direction)

- Consistent income (5-15% annually is realistic)

- Best liquidity in the market (always get good fills)

- Flexible sizing (scale precisely with my account)

What they don’t give me:

- Home run returns (this is income, not speculation)

- Passive hands-off trading (requires weekly monitoring)

- Protection from sustained trends (range-bound strategy)

If you have $25k+, the discipline to follow rules, and patience for modest consistent returns, Iron Condors on SPY can be a valuable addition to your income strategy.

Next Steps #

- Read the Iron Condor Entry Checklist - Every criterion must pass

- Study the Workflow Guide - Learn my daily/weekly routine

- Print the 1-Page SOP - Keep it visible when trading

- Paper trade for 60 days - This is more complex than CSPs; practice first

- Start with 1 contract - Your first real trade should be small

Disclaimer: This is educational content based on my personal experience and research. Options trading involves significant risk and is not suitable for all investors. Iron Condors can lose significant capital in volatile or trending markets. Past performance does not guarantee future results. Always do your own research.

Sources: